The economic opportunity pillar is designed to eliminate the Black community’s barriers to economic access, equity, and opportunity.

The legislation addresses banking and investment, economic mobility, small business and entrepreneurship, state procurement and the Business Enterprise Program, industry-specific equity, environmental equity, housing and land use, pay equity and workers’ rights, and capital investments.

Economic Access, Equity and Opportunity Pillar Package Fact Sheet

Sponsor: Senator Christopher Belt (D-Centreville)

Senate Bill 1980

- Property Tax Code

- Each person purchasing property in counties with 3 million or more inhabitants must pay a fee to the respective County Collector for each item purchased, plus an additional sum.

- Housing Authorities Act

- Housing authorities must track data from public housing applicants regarding the total number of applicants, the number of applicants on which a criminal background check was run, and the number of applicants denied, among other things.

- This report must be submitted to the Illinois Criminal Justice Information Authority, which must then compile the reports and report them to the General Assembly and public.

- Changes the word “felon” to “individual with felony conviction” on statutory provisions.

- Requires housing authorities to make individual assessments on the reasonability of concluding whether an applicant would constitute a threat or engage in unlawful activities before refusing to certify or recertify applicants who have been convicted of a controlled substance related offense.

- Requires housing authorities to inform applicants of an impending denial of certification or recertification as well as their right to an impartial hearing to demonstrate that the individual’s particular circumstances warrant they not be denied.

- Requires housing authorities, when conducting assessments, to consider each individual’s mitigating circumstances and provides examples of appropriate circumstances.

Senate Bill 1480

- Human Rights Act

- Prohibits an employer from using conviction record as the basis for hiring discrimination against an applicant unless the employment in question and the criminal offense have “substantial relationship,” or granting or continuing employment poses a safety risk.

- Allows the employer to consider duration, amount, circumstances and severity of convictions, the individual’s age at the time of conviction, and evidence of rehabilitation efforts when making a decision based on conviction record.

- Requires the employer to provide written notice to applicants who’s hiring decisions are denied based on criminal conviction and allow the individual 5 days to respond before a final decision is made.

- Business Corporation Act

- Requires any employer who must file an Employer Information Report with the Equal Employment Opportunity Commission must also submit the same data from that repot to the Illinois Secretary of State.

- Equal Pay Act

- Prohibits the Prohibits the state from contracting with a private business with more than 100 employees that does not have an equal pay certificate.

- An equal pay certificate certifies that

- The company is in compliance with various federal equal rights statutes.

- The average compensation for female employees is not consistently below the average compensation for male employees.

Senate Bill 1608

- State Contract Goals

- Increases Business Enterprise for Minorities, Women, and Persons with Disabilities Act goals for each category.

- Procurement Code

- Requires competitive sealed bids to include commitment to diversity, in addition to price.

- Provides that vendors are not eligible for contract renewals when that vendor has failed to meet goals, unless the state agency has determined that good faith efforts to were made.

- Provides diversity training for procurement staff.

- Requires a state agency or institute of higher learning to file an annual report on its contracts with businesses under BEP, including plans to increase diversity.

- Illinois SBIR/STTR Matching Funds Program

- Reinstates the Illinois Small Business Innovation Research (SBIR) and Small Business Technology Transfer (STTR) Matching Funds Program, which awards grants to startup and research businesses that receive federal grants.

- African Descent-Citizens Commission

- Creates a commission to address issues relating African American descendants of slavery mired in poverty.

- Deposit of State Moneys Act

- Permits the Illinois Treasurer to invest or reinvest certain funds in Community Development Financial Institutions and Minority Depository Institutions.

- Race and Gender Wage Reports

- Amends the CMS Law of the Civil Administrative Code of Illinois to provide that each state agency and institution of higher education shall file an annual report with DCEO giving information about wage earnings of state employees by both race and gender.

- Community Development Loan Guarantee Act

- Provides that the State Treasurer may create a community loan guarantee program with up to $10 million to assist in covering losses of certain development projects.

- Illinois Community Reinvestment Act

- Requires covered financial institutions to meet certain financial services needs of local communities, including low- and moderate-income neighborhoods and areas where there is a lack of access to safe and affordable banking.

- Commission on Equity and Inclusion

- Creates a commission to oversee procurement, with a focus on minority inclusion and diversity.

- Technology Development Act

- Increases the amount of earnings from the Technology Development Account and Technology Account II that can be transferred to the Technology Development Fund and allows them to be used to promote the growth of technology jobs in communities of color.

- Child Care

- Provides that IDHS shall update the Child Care Assistance Program Eligibility Calculator on its website to include a question about whether a family is applying for the first time or trying to redetermine eligibility.

Senate Bill 1792

- Farmer Equity Act

- Requires the Department of Agriculture to conduct a study by Jan. 1, 2022, which examines racial and economic disparities associated with farm ownership and operations.

- Cannabis Equity Commission

- Creates a commission to track and make recommendations relating to minority participation in the cannabis market.

- Predatory Loan Prevention Act

- The act will protect consumers from predatory loans, based on the federal Military Lending act by

- Amending the Payday Loan Act to create more protections for consumers and require more reporting from lenders.

- Including changes to the types of licenses lenders need, actions prohibited by lenders, and changes to loan terms.

- Capping the interest rate for installment loans at 36%.

- Amending the Consumer Installment Loan Act to make changes to the amount that can be charged on an installment loan.

- Removing the provisions exempting Small Consumer Loans from different reporting and interest rate rules.

- Barber, Cosmetology, Esthetics, Hair Braiding, and Nail Technology Act of 1985

- Requires the Department of Financial and Professional Regulation to evaluate discrimination in the state’s beauty supply industry

- The act will protect consumers from predatory loans, based on the federal Military Lending act by

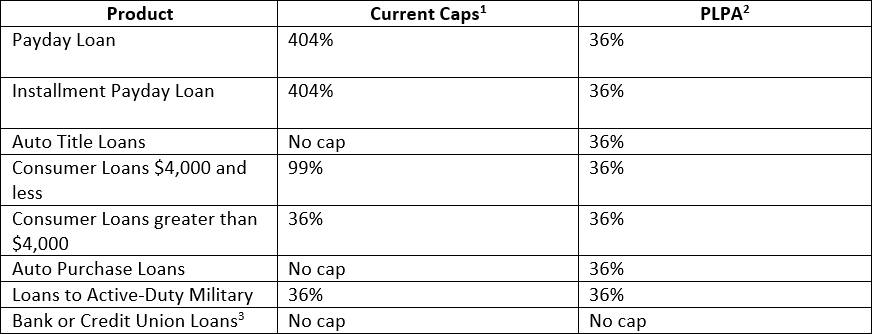

Table of Rate Caps (Before and After)

[1] All rates are annual percentage rates (APRs) calculated according to the Truth In Lending Act except for loans made to active-duty military, which are calculated according to the Military Lending Act.

[1] All rates are annual percentage rates (APRs) calculated according to the Truth In Lending Act except for loans made to active-duty military, which are calculated according to the Military Lending Act.

[2] All rates are annual percentage rates (APRs) calculated according to the Military Lending Act.

[3] National banks and credit unions are not subject to state rate caps.

Payday loan: Single-payment loan due on the borrower’s next payday.

Installment payday loan: A payday loan payable in installments with a maximum term of 120 days. Payments are due on the borrower’s payday.

Auto Title Loan: Loan secured by borrower’s car title. Average term around 20 months. Failure to pay can result in repossession.

Consumer Loans $4,000 and less (technically “small consumer loans”): Average term about one year.

Consumer Loans greater than $4,000: Terms typically 2-5 years.

Auto Purchase Loans: Loan to purchase an automobile. Average term is around 6 years. Failure to pay can result in repossession.

Loan to Active-Duty Military: The Military Lending Act covers most consumer loans, but the Act protects only active-duty members and their dependents. A veteran, for example, is vulnerable to predatory loans.